On November 6, 2018 the James A. Garfield Local Schools will be placing a 10-year, 1.5% Earned Income Tax on the ballot. With the passage of this issue, the district intends to let the 5.25 Mill Emergency Levy expire in 2019. This issue will generate operating funds to sustain current educational programming.

Listed below are the answers to the questions that have been received from the Garfield Community. Residents are encouraged to attend the public information session for the Earned Income Tax Issue on Sept 16 at 4 pm in the Iva L. Walker Auditorium at the high school. Attendees will receive information about the upcoming Earned Income Tax Issue, and have the opportunity to have their questions answered. A livestream of the session will also be provided, and online questions will be accepted during or after the Q&A portion.

1. Why is the District asking for money?

The district’s current financial position will result in a deficit in 2020. Despite cuts and cost-saving measures the District will need to generate additional funds to eliminate the deficit.

• Revenue has been almost flat since 2016.

• Revenue has grown less than one-half percent the past two years.

• State funding is 45% of the district’s budget and has been flat since July 1, 2016 and the current state funding formula reflects no growth through at least 2019.

• Local real estate tax revenue declined slightly since 2016 and is projected to experience only slight growth through at least 2019.

The ongoing impact of flat revenue quickly consumes one-time cash balance reserves and the district is projecting a negative cash balance next fiscal year. The cost of providing services has exceeded revenue the past two years.

Garfield has been left behind by the state. Because we have been left with the responsibility of keeping our schools excellent, we are faced with a choice to continue our tradition of excellence that make our schools the pride of our community or go down the road that many of our neighboring districts have been forced to do – make cuts to our schools that impact our kids.

2. When was the last time the District asked for new funds?

The District has not asked for additional funds in 14 years. The last time voters approved an increase was in 2004.

3. What is a School District Earned Income Tax?

A School District Earned Income Tax is a tax applied to residents who live in the school district on their earned income/tips or self-employment income.

4. How is the tax collected?

School District Earned Income Taxes are required by the State of Ohio to be deducted directly from paychecks by any employer in Ohio or employers doing business in Ohio.

5. What are the penalties for failure to withhold the tax?

The amounts of penalty and interest for failure to withhold the SDIT are the same as for failure to withhold the state income tax. The employer must request that employees furnish the name of the school district in which they reside. If the information furnished by the employee is incorrect and the tax is not withheld properly, the obligation for payment of the tax plus penalties and interest falls totally on the individual. Failure to withhold by fault of the employer shifts payment of the penalty and interest to the employer, but does not relieve an employee from the liability for the tax.

6. Are employers required to withhold the School District Income Tax?

Yes. The Ohio Department of Taxation has contacted each business in Ohio and informed them of their obligation to withhold the tax and make payments of the withheld taxes through the Ohio Business Gateway (OBG). A list of school districts levying the tax and corresponding tax rates is provided to each business along with withholding tables and computerized withholding formulas. Employers must ask employees in which school district they reside. Employees will be responsible for reporting the correct school district to the employer.

An exception to this rule is in regard to Federal Government employees. The State of Ohio cannot require the Federal Government to withhold income taxes. Therefore, these individuals would be required to pay the SDIT either quarterly or annually if withholding is not done voluntarily.

7. I am a senior citizen receiving a pension, do I have to pay the tax?

No. Pensions are not taxable under a school district earned income tax.

8. What types of income are NOT subject to an Earned Income Tax?

The following sources of income are NOT taxable under an Earned Income Tax:

- Social Security

- Interest

- Dividends

- Unemployment Compensation

- Taxable Scholarships and fellowships

- Pensions

- Annuities

- IRA distributions

- Capital Gains

- State and local bond interest (except that paid by Ohio governments)

- Federal bond interest exempt from federal tax but subject to state tax

- Alimony received

- and all other sources.

9. Why did the district decide to pursue an Earned Income Tax?

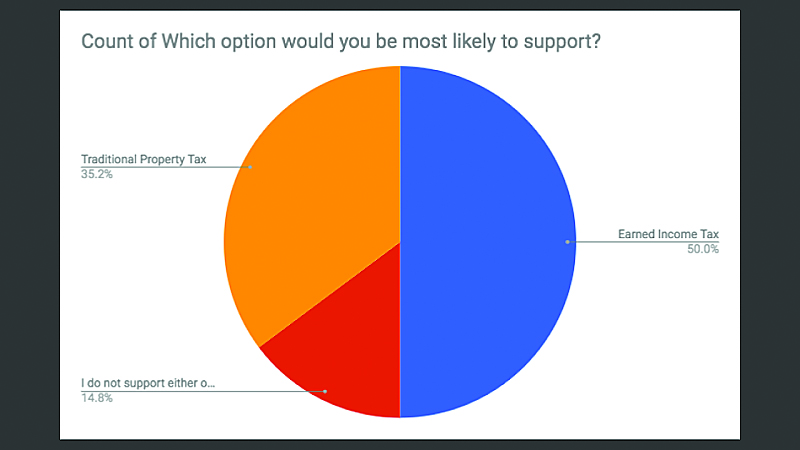

After analyzing data on our average home value, district property taxes, and makeup of community (age, rent vs. own, income, home value, children in the district, etc) the District surveyed 1,000 random voters to determine whether they preferred a traditional property tax or an earned income tax. The results clearly favored the Earned Income Tax (59%). Further, after analyzing the impact of the Earned Income Tax it had the least impact on the largest number of residents (based on age, income and home value).

10. Why will the district allow the Emergency Operating Levy to expire in 2019?

The district does not want to ask for anymore money than what we need to continue operating a our current level of service. Garfield is currently has some of the lowest property tax rates in Portage County (based on voted millage). The committee felt it was important to protect that in order to remain an attractive place for young families to build/buy their homes. Allowing the emergency operating levy to expire will keep Garfield among the most affordable places to live in Portage County. By taking this action we reduce the property tax burden for all residents.

11. What kind of savings will I see in my property taxes when the Emergency Levy expires?

The average homeowner ($155,000 home) will save $256.33/year on their property taxes.

12. What will the new Earned Income Tax Cost me?

The average wage/salary in Garfield $41,745/year. The 1.5% Earned Income Tax would cost the average taxpayer $24.08/pay (based on average salary and 26 pays/year).

The tax information presented above and for planning is referencing average wage and salary income at $41,745. The tax information used to generate average wage and salary income is from the Internal Revenue Service (IRS). Data used includes all IRS returns filed from the 44231 zip code that reported wage and salary income. While every situation is different, this is the average based on single, joint and head of household returns filed, which is the most accurate, granular information available to us.

13. I already pay an income tax where I work, how is the School District Earned Income Tax impacted by this?

They are not related. Only residents of the Garfield School District will pay the 1.5% Earned Income Tax, and funds collected through it are not shared with any other entity.

14. Is the School District Earned Income Tax related at all with RITA (Regional Income Tax Agency)?

No. The Regional Income Tax Agency provides services to collect income tax for municipalities in the State of Ohio, not school districts. The State of Ohio requires all employers in the State to withhold School District Earned Income Tax from paychecks.

These withholdings are sent directly to the Treasurer of the State of Ohio and distributed to the appropriate school district.

15. Do parents/guardians of open enrollment students pay the tax?

No. State law prohibits school districts from assessing taxes to non-residents of the school district. The earned income tax is only paid by residents of the school district. Open enrollment allows a student to attend another school tuition-free. However, the school district receives $6,020 per student from the Ohio Department of Education for each student who is open enrolled to Garfield. Open enrollment allows the school district to operate at maximum efficiency by lowering the fixed costs per pupil. Examples of fixed costs are salaries, textbooks, utilities, etc.

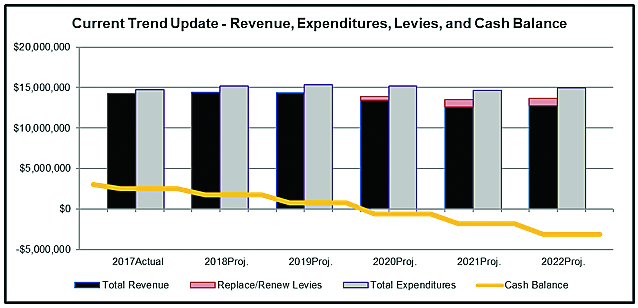

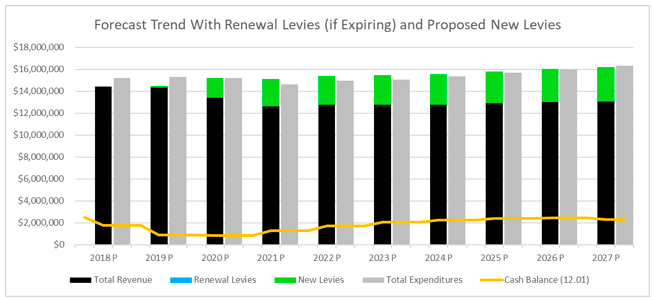

16. How long will these additional funds last?

The following graph shows how funds from the Earned Income Tax would impact the District’s financial position. It is our goal to be off the ballot for at least another 10 years.

17. What budget cuts can be made?

In 2017 the district spent 2.8% less per student than similar districts and 17.4% less than the state average. The district’s administrative costs were lower than similar districts and instructional expenditures could not keep up with needs and were less than similar districts and the state average.

We cannot settle for cuts to be the only answer for our schools, now or in the future. We take pride in the excellence of our schools and know that they are the cornerstone of our community. Our community is uniting this November to support and preserve the things that make our schools excellent. By passing the 1.5% Earned Income Tax, we are ensuring our schools will remain excellent for future generations of Garfield graduates.

This November, WE MUST UNITE to preserve the cornerstone of our community – our schools.

18. How did the District decide to pursue the Earned Income Tax?

An earned income tax will help balance the district’s property tax levies. This was concluded by a committee of community members assembled to help decide the best option to solve the upcoming $1.4M deficit.

The committee examined data that included a detailed review our finances, a performance audit done by the Ohio Auditor of State, demographic data, income data, and property tax data. The committee wanted additional input from the community on whether to pursue a traditional property tax or an earned income tax to eliminate the $1.4M deficit.

Voter information was obtained through the Portage County Board of Elections. A list of over 2,500 probable voters was used to randomly select 1,000 households. An online survey was created and a postcard was sent to the 1,000 random households with a link to this survey. Results from this survey showed that the earned income tax was preferred.

19. How many people in our community are there that own property compared to how many work?

Current data pulled from the Portage County Auditor and 2016 data pulled from the Ohio Department of Taxation show the following breakdown of property owners and tax returns filed (workers) in the Garfield School District.

Property Owners (unique parcels): 2,559

Workers (tax returns filed)*: 4,177

*Total returns filed joint, single and head of household. This is a minimum number as each return filed as joint are only counted as one worker. Actual number of workers earning an income may be higher.

Data for the above information can be found by visiting the Ohio Department of taxation and the Portage County Auditor links below. https://www.tax.ohio.gov/tax_analysis/tax_data_series/school_district_data/publications_tds_school/Y2TY16.aspx

http://portagecountyauditor.org/Search.aspx

20. What happens if I have more than one person earning an income in my home?

The 1.5% Earned Income Tax will be applied to each wage earner. It is important to note that the tax is NOT increased when applied to more than one wage earner.

21. How many senior citizens are there in the District that will not pay?

Based on the 2016 Ohio Department of Taxation records, 17% of income tax returns filed utilized the Senior Citizen Credit. This is the most accurate way to determine how many senior citizens will not pay as there may be senior citizens who are still earning an income.

22. How will this impact people that rent in the District?

Renters living within the Garfield Schools will be required to pay the Earned Income Tax if they are working.

23. What will the language on the November Ballot look like?

The ballot language proposed will look as follows:

JAMES A. GARFIELD LOCAL SCHOOL DISTRICT PROPOSED SCHOOL DISTRICT INCOME TAX (ADDITIONAL) (A Majority Affirmative Vote is Necessary for Passage.) Shall an annual income tax of one and one-half of one percent (1.50%) on the earned income of individuals residing in the school district be imposed by James A. Garfield Local School District, for 10 years, beginning January 1, 2019, for the purpose of current expenses? FOR THE TAX AGAINST THE TAX

NOTE REGARDING FORM OF BALLOT:

Section 5748.03 of the Revised Code specifies the form of ballot to be used. This form has been prepared based upon those requirements.

24. Can the district charge open enrollment students a fee to attend Garfield?

No. Created in 1989, intra- and inter-district open enrollment is the process by which students can enroll into another school building or another school district on a tuition free basis. Inter-district open enrollment refers to native students of a district enrolling in another district by following that district’s open enrollment policies and procedures. Students enrolled under an open enrollment policy must be allowed to attend tuition free. Currently, the State provides Garfield $6,020.00 for every open enrollment student who attends. The State of Ohio determines a state tuition fee each year and this cost is currently $4,393.55. It is more cost effective for the District to allow open enrollment and receive $6,020.00 per student than to select to accept tuition and receive $4,393.55.

25. What is the history of the Emergency Levy the District plans to let expire at the end of 2018 (if the income tax issue is passed)?

The JAG Emergency Levy for $925,000 was approved by voters for the first time in November 2004. The levy was for calendar year 2004 and voters starting paying the levy amount with the first half payment due in February 2005. Effectively running from 1/1/2004 through 12/31/2008, but paid 1/1/2005 through 12/31/2009 because property taxes are paid the following year.

The first renewal was November 2008, running from 1/1/2009 through 12/31/2013, but paid 1/1/2010 through 12/31/2014.

The second renewal was November 2013, running from 1/1/2014 through 12/31/2018, but paid 1/1/2015 through 12/31/2019.

The levy will expire on 12/31/2018, but Portage County residents do not pay the taxes for calendar year 2018 until calendar year 2019- typically in February and July.

26. What will these funds be used for?

The additional $1.4M raised by the passage of the Earned Income Tax will be used to continue current educational programs (i.e. course offerings, technology, curriculum), school safety (i.e. cameras, door upgrades) and maintenance of our aging facilities (i.e. our high school roof is over 30 years).

27. Have you taken into account what the new property values are going to do as far as an increase in money collected?

Yes. In the planning stages of this issue we were anticipating a 10% increase in property value prior to the Portage County Auditor releasing the actual increase. The increase released by the Portage County Auditor to the district came in at 9% for the District. The additional $1.4M needed to eliminate our deficit was determined with this increase built into the projections.

28. Are there talks of cutting buses or pay to play sport if this don’t pass or will you wait and try again or try for a levy?

The board of education is confident this issue will pass based on the feedback we have received from surveys and feedback at presentations thus far. However, it would not be responsible to move forward without planning for the worst, which would be the issue failing. The board will be meeting in September to discuss a contingency plan that will certainly include a list of options to consider. What we do know is that if the issue fails the board will be forced to eliminate an additional $1.4M from the budget. To get to that number all the items listed above (busing and pay to play) would have to be considered.

At the meeting, the board will also be evaluating which option they would feel is most likely to get support if this issue does not pass.

We are confident this issue will pass and we will not be forced to enact reductions that would negatively impact our students.

29. Who is eligible to vote on this matter?

Your voter registration will determine where you vote, which should be based on your home address. Wherever you vote for any election will determine whether or not you are eligible to vote on this matter. If you are registered in the Garfield School District you will be eligible to vote, but if you live outside the district you will not.

30. How will this tax impact a business/commercial property owner that operates within the Village. Will this Tax be set up same as the village income tax? Will all employees of the business, regardless of where they reside, be subject to this tax?

When this issue passes the District will allow the 5.25 Mill Emergency Operating Levy to expire in 2019, so you would receive a reduction on the property tax you pay on the property you own within the district.

A School District Earned Income Tax is different than a village income tax. Municipal taxes are paid directly to the municipality (Village of Garrettsville) or RITA. School District Earned Income Taxes are considered a State tax and are withheld as an additional State Tax and are sent to the Treasurer of State by the employer and they distribute to the school district on a quarterly basis. The School District Earned Income Taxes are only withheld for employees who reside in the Garfield District.

31. How would a property tax renewal equate to the 1.5% earned income in regards to money collected per year? Is that the next option if this levy fails?

The renewal of the emergency levy that is due in 2019 generates $925,000 annually. The district’s revenue has been almost flat since 2016 and our operating costs are increasing. Even with reductions/cost saving measures that equate to over $6.1M over the past five years, we still fall $1.4M short annually without the issue (that is assuming the passage of the property tax renewal). The 1.5% would generate the additional $1.4M needed and replaces the $925,000 property tax.

32. If I am paying the tax will both of my children be required to pay it if they are away at college working part-time?

Since they are a resident of Garrettsville even though they are not living at home, it depends on how your child fills out their State Tax Return. When your child prepares their Ohio return, they have to state on the form the Ohio school district in which they were a resident for the “majority of the year”. If they list Garfield, this will trigger them to file SD-100. If they state otherwise, the SD-100 may not be triggered. It would be important to look at which school district they are living in when at college. If they are living in a district that has an income tax they would pay at that location to that district. Below is a link to a list of districts in Ohio that have School District Income Taxes (about 1/3 of Ohio Districts have them and the list is growing quickly).

Array

33. When deteriming to place an Earned Income Tax on the ballot, did the committee take into account those individuals that live paycheck to paycheck and how it would impact them?

Yes, we did consider those individuals living paycheck to paycheck, and it was one of the reasons the Earned Income Tax is the most responsible way to solve our problem. One of the most important points to remember is that if a resident falls on hard times (i.e. loses a job or takes a pay reduction) they will NEVER pay more than 1.5%. So, as pay decreases so does the contribution. This is NOT possible with property taxes. That same person would still be responsible for the payment of their property taxes. In addition to that, our retired residents who have no means of increasing their income are not burdened by the Earned Income Tax.

34. How does the tax work if a resident has a full-time job which provides a W-2 and also a small business that affects the AGI. At the end of the year if the resident has paid in more tax than what is due is there a refund like the state of Ohio return?

With a School District Earned Income Tax, you are taxed on the earned wages or self-employment wages. However, because of the Ohio Small Business Deduction of $250,000, the School District Earned Income Taxes are only applied to self-employment wages above the $250,000.

If you small business shows a loss your taxable income will be lowered for Federal and State tax rates but not for the purposes of the School District Earned Income Tax.

There are many different parts to how these situations are calculated and while we are getting this information from the Ohio Department of Taxation you should always consult your local tax preparer to confirm your situation.

35. I am a retiree receiving both social security and a monthly pension. My neighbor told me that I am going to have to pay the Earned Income Tax as well as my property taxes to support the schools.

This is an incorrect statement. As a retiree receiving social security and a pension, your monthly income will NOT be taxed. (see questions 7,8 & 9) When this issue passes the District will allow the 5.25 Mill Emergency Operating Levy to expire in 2019, so you would receive a reduction on the property taxes you pay beginning in tax year 2020. (see questions 10 & 11)